Accounting Q&A Section

Questions and answers in accounting

How is Net Income converted to Cash Flows from Operating Activities using the indirect method?

The indirect method starts with Net Income and adjusts for: 1) Non-cash items, 2) Changes in working capital, 3) Gains/losses on asset sales to arrive at Operating Cash Flow.

Read more → Jan 7, 2026

How is the Statement of Cash Flows used to assess the quality of earnings?

Cash flow statement helps assess earnings quality by comparing Net Income to Operating Cash Flow, examining cash sources, analyzing adjustments, and evaluating consistency.

Read more → Jan 7, 2026

What is net working capital? Why is it important?

Net Working Capital = Current Assets - Current Liabilities. It's important for measuring liquidity, funding operations, indicating efficiency, and assessing creditworthiness.

Read more → Jan 7, 2026

What is horizontal and vertical analysis of financial statements?

Horizontal analysis examines changes over time (trend analysis), while vertical analysis examines relationships within a period (common-size statements showing percentages).

Read more → Jan 7, 2026

What is financial leverage and operating leverage?

Operating leverage uses fixed operating costs to magnify EBIT changes from sales changes. Financial leverage uses debt to magnify net income and ROE changes from EBIT changes.

Read more → Jan 7, 2026

What is break-even analysis? How is the break-even point calculated?

Break-even analysis determines sales level where total revenue equals total costs (zero profit). BEP in units = Fixed Costs/Contribution Margin per unit.

Read more → Jan 7, 2026

How are solvency/leverage ratios (Debt-to-Equity, Interest Coverage) calculated and interpreted?

Debt-to-Equity = Total Liabilities/Equity, Interest Coverage = EBIT/Interest Expense. These measure long-term financial stability and ability to meet obligations.

Read more → Jan 7, 2026

How are activity ratios (Inventory Turnover, Days Sales Outstanding) calculated and interpreted?

Inventory Turnover = COGS/Average Inventory, DSO = 365/Receivables Turnover. These measure efficiency in managing inventory and collecting receivables.

Read more → Jan 7, 2026

How are profitability ratios (ROA, ROE) calculated and interpreted?

ROA = Net Income/Average Total Assets (asset efficiency), ROE = Net Income/Average Equity (owner return). DuPont analysis breaks ROE into margin, turnover, and leverage components.

Read more → Jan 7, 2026

How are liquidity ratios (Current, Quick) calculated and interpreted?

Current Ratio = Current Assets/Current Liabilities, Quick Ratio = (Cash + Marketable Securities + Receivables)/Current Liabilities. Both measure short-term debt-paying ability.

Read more → Jan 7, 2026

What are the main financial ratios (liquidity, profitability, activity, solvency)?

Main financial ratio categories: 1) Liquidity (Current, Quick), 2) Profitability (ROA, ROE, margins), 3) Activity (turnover ratios), 4) Solvency (debt ratios, interest coverage).

Read more → Jan 7, 2026

Why is the Statement of Cash Flows important to users?

The Statement of Cash Flows is crucial for assessing liquidity, evaluating earnings quality, revealing financial strategy, predicting future cash flows, identifying red flags, and supporting valuation.

Read more → Jan 7, 2026

What is the difference between the direct and indirect methods for preparing the Operating Activities section?

Direct method shows actual cash receipts and payments, while indirect method starts with Net Income and adjusts to cash flow. Both give same result but present information differently.

Read more → Jan 7, 2026

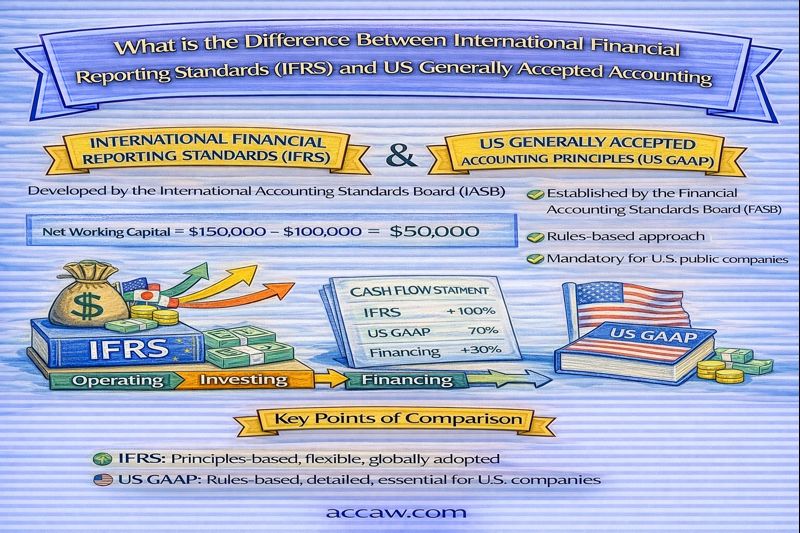

What is the difference between International Financial Reporting Standards (IFRS) and US Generally Accepted Accounting Principles (US GAAP)?

Key differences: IFRS is principles-based, used globally; US GAAP is rules-based, used in US. Differences exist in inventory (LIFO), development costs, inventory write-down reversals, and presentation.

Read more → Jan 7, 2026

What are the three sections of the Statement of Cash Flows (Operating, Investing, Financing)?

The Statement of Cash Flows has three sections: 1) Operating Activities (core business), 2) Investing Activities (asset purchases/sales), 3) Financing Activities (debt/equity transactions).

Read more → Jan 7, 2026

What is the difference between Net Income and Cash Flow?

Net Income is accrual-based profit (revenues - expenses), while Cash Flow is actual cash movement. A company can be profitable but have negative cash flow, or vice versa.

Read more → Jan 7, 2026

How do different accounting policies (e.g., FIFO vs. LIFO) affect the income statement?

Accounting policy choices like inventory method (FIFO vs LIFO) and depreciation method directly affect COGS, depreciation expense, and thus net income reported on the income statement.

Read more → Jan 7, 2026

What is EBITDA? Why is it important?

EBITDA = Earnings Before Interest, Taxes, Depreciation, and Amortization. It's important as a proxy for operating cash flow, comparison tool, and valuation metric, though it has limitations.

Read more → Jan 7, 2026

How is deferred income tax calculated? What is the difference between a Deferred Tax Asset and a Deferred Tax Liability?

Deferred tax arises from temporary differences between accounting and tax bases. DTA represents future tax savings, DTL represents future tax payable. Calculated as Temporary Difference × Tax Rate.

Read more → Jan 7, 2026

What is an "adjusting entry"? Why is it necessary?

Adjusting entries are journal entries made at period-end to update accounts and ensure compliance with accrual accounting. They record internal economic events not captured by routine entries.

Read more → Jan 7, 2026

What is the difference between the comprehensive income statement and the traditional income statement?

Traditional income statement shows only net income, while comprehensive income statement includes both net income and other comprehensive income items that bypass the income statement.

Read more → Jan 7, 2026

What is Comprehensive Income? What are its components?

Comprehensive Income = Net Income + Other Comprehensive Income (OCI). OCI includes items like foreign currency translation adjustments, unrealized gains/losses on certain investments, and revaluation surplus.

Read more → Jan 7, 2026

What are extraordinary and non-recurring items? How are they presented?

Under current IFRS and US GAAP, extraordinary items classification is eliminated. Unusual or infrequent items are reported as part of continuing operations with separate disclosure.

Read more → Jan 7, 2026

How are gross profit margin, operating profit margin, and net profit margin calculated and interpreted?

Gross margin = Gross Profit/Revenue, Operating margin = Operating Income/Revenue, Net margin = Net Income/Revenue. Each measures profitability at different stages of operations.

Read more → Jan 7, 2026

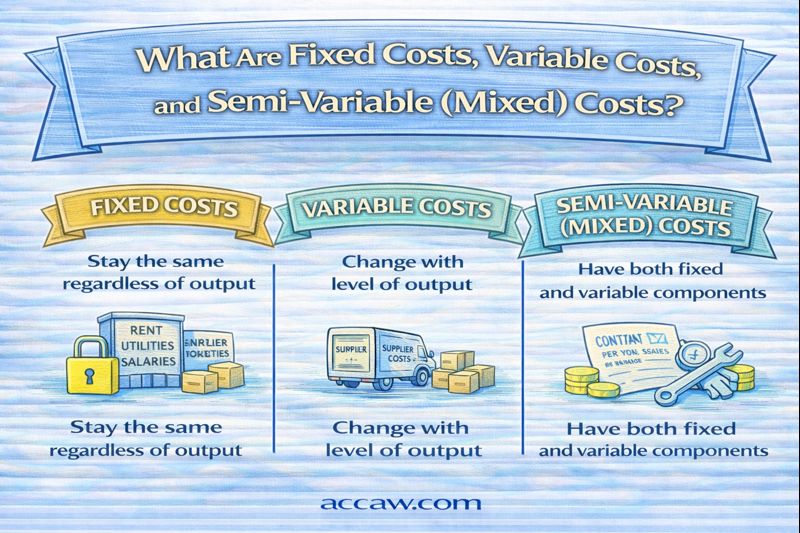

What are fixed costs, variable costs, and semi-variable (mixed) costs?

Fixed costs remain constant regardless of activity level, variable costs change proportionally with activity, and semi-variable costs have both fixed and variable components.

Read more → Jan 7, 2026

What are analytical procedures in an audit?

Analytical procedures are evaluations of financial information through analysis of plausible relationships. Used in audit planning, substantive testing, and final review stages.

Read more → Jan 7, 2026

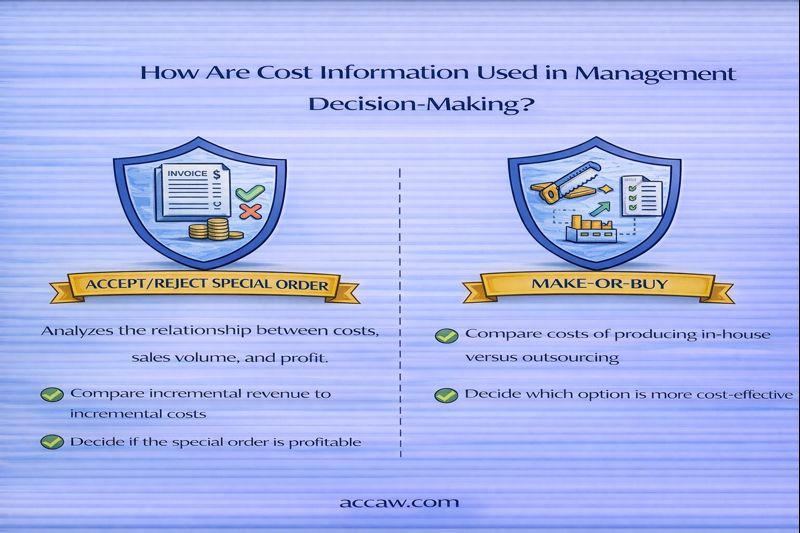

How are cost information used in management decision-making (accept/reject a special order, make-or-buy)?

Cost information supports decisions like special orders (consider incremental costs/revenues) and make-or-buy (compare relevant costs). Focus on relevant costs that differ between alternatives.

Read more → Jan 7, 2026

What is Cost-Volume-Profit (CVP) analysis?

CVP analysis examines relationships between costs, volume, and profit. Key components: contribution margin, break-even point, target profit analysis, margin of safety, operating leverage.

Read more → Jan 7, 2026

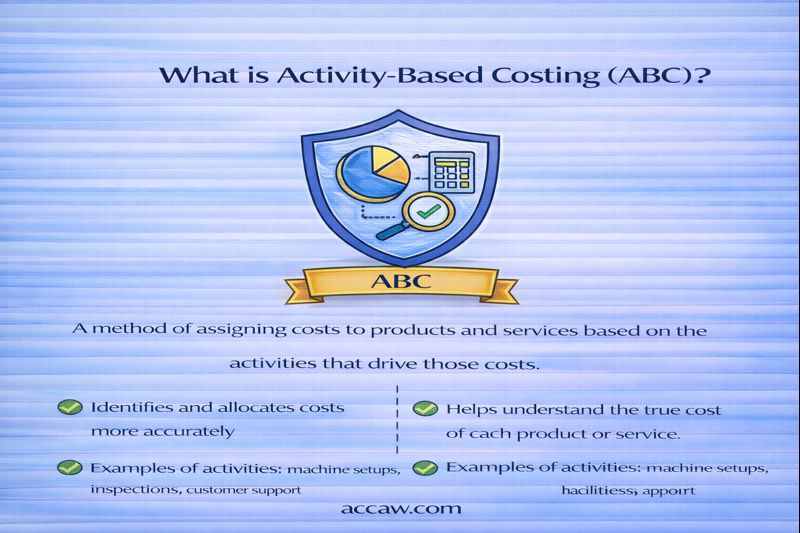

What is Activity-Based Costing (ABC)?

ABC is a costing method that allocates overhead based on activities that drive costs, using cost drivers. Provides more accurate product costing than traditional methods.

Read more → Jan 7, 2026

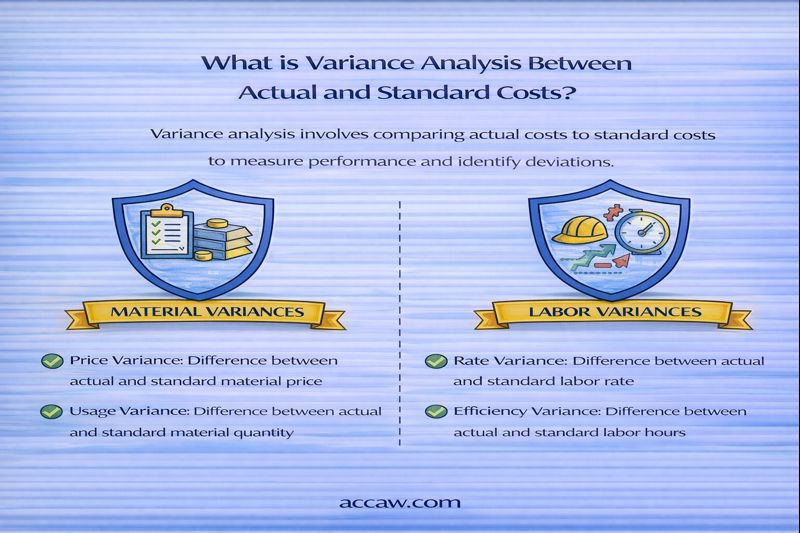

What is variance analysis between actual and standard costs (material, labor variances)?

Variance analysis compares actual to standard costs. Material variances: Price and Quantity. Labor variances: Rate and Efficiency. Used for cost control and performance evaluation.

Read more → Jan 7, 2026

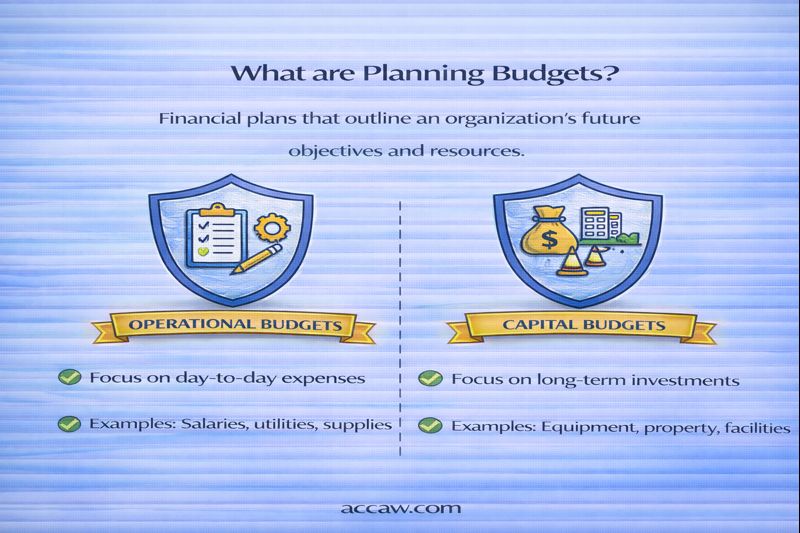

What are planning budgets? What are their types (operational, capital)?

Planning budgets are quantitative financial plans. Types: 1) Operating budgets (short-term revenue/expense plans), 2) Capital budgets (long-term investment plans).

Read more → Jan 7, 2026

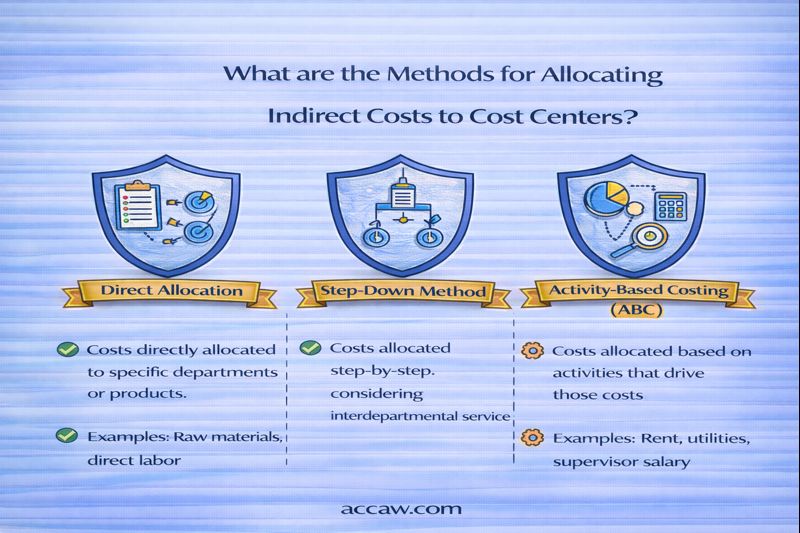

What are the methods for allocating indirect costs to cost centers?

Common allocation methods: Direct Labor Hours, Direct Labor Cost, Machine Hours, Units of Production, Square Footage. Activity-Based Costing provides more refined allocation.

Read more → Jan 7, 2026

What is the difference between direct costs and indirect costs?

Direct costs are easily traceable to specific cost objects (e.g., direct materials for a product). Indirect costs cannot be easily traced and must be allocated (e.g., factory rent).

Read more → Jan 7, 2026

How are prime costs and conversion costs calculated?

Prime Cost = Direct Materials + Direct Labor. Conversion Cost = Direct Labor + Manufacturing Overhead. Both are important manufacturing cost classifications.

Read more → Jan 7, 2026

What are the basic systems for cost accumulation (Job Order Costing, Process Costing)?

Job Order Costing accumulates costs by specific jobs/batches (custom products), while Process Costing accumulates costs by processes/departments (mass-produced homogeneous products).

Read more → Jan 7, 2026

What is the difference between cost accounting and financial accounting?

Cost accounting focuses on internal cost information for management decisions, while financial accounting focuses on external financial reporting for stakeholders following standards.

Read more → Jan 7, 2026

What are working papers and why are they important in the audit process?

Audit working papers document procedures performed, evidence obtained, and conclusions reached. They are important for evidence, review, supervision, continuity, and legal protection.

Read more → Jan 7, 2026

What is the concept of "materiality" in auditing?

In auditing, materiality is information that could influence users' economic decisions. It guides audit planning, procedure extent, and evaluation of misstatements.

Read more → Jan 7, 2026

What is the difference between Cost of Sales (Cost of Goods Sold) and Operating Expenses?

Cost of Sales is directly traceable to products sold (variable with sales), while Operating Expenses support overall business operations and are often fixed or semi-variable.

Read more → Jan 7, 2026

What is audit risk? What are its types (Inherent, Control, Detection)?

Audit risk is risk auditor expresses inappropriate opinion when statements are materially misstated. Components: Inherent Risk × Control Risk × Detection Risk (AR = IR × CR × DR).

Read more → Jan 7, 2026

What are the main components of internal control?

Main internal control components (COSO framework): 1) Control Environment, 2) Risk Assessment, 3) Control Activities, 4) Information & Communication, 5) Monitoring Activities.

Read more → Jan 7, 2026

What opinion can an auditor issue on the financial statements? (Clean, Qualified, Adverse, Disclaimer)

Audit opinion types: 1) Unmodified (Clean), 2) Qualified (except for), 3) Adverse (do not present fairly), 4) Disclaimer (cannot express opinion).

Read more → Jan 7, 2026

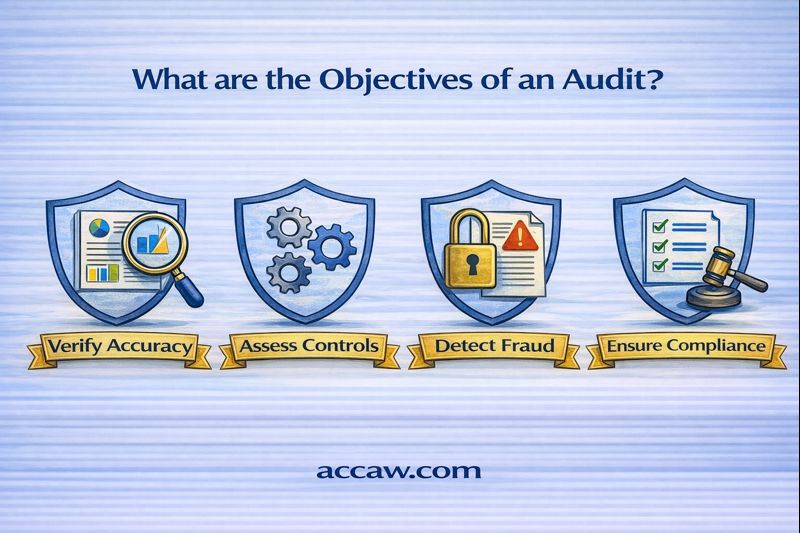

What are the objectives of an audit?

Primary audit objective: express opinion on whether financial statements present fairly in accordance with framework. Specific objectives include obtaining reasonable assurance and reporting findings.

Read more → Jan 7, 2026

What is the difference between internal audit and external audit?

Internal audit is an independent assurance function within organization focusing on risk management and controls. External audit is independent examination of financial statements by external auditors.

Read more → Jan 7, 2026

What is the financial reporting standard for small and medium-sized entities (SMEs)?

IFRS for SMEs is a simplified, self-contained standard for entities without public accountability. It reduces complexity, disclosure requirements, and measurement options compared to full IFRS.

Read more → Jan 7, 2026

What is the financial instruments standard (IFRS 9)?

IFRS 9 covers: 1) Classification/measurement based on business model and cash flow characteristics, 2) Expected credit loss impairment model, 3) Hedge accounting requirements.

Read more → Jan 7, 2026

What is the revenue recognition standard for contracts with customers (IFRS 15)?

IFRS 15 provides a five-step model for revenue recognition: 1) Identify contract, 2) Identify performance obligations, 3) Determine price, 4) Allocate price, 5) Recognize revenue when obligations satisfied.

Read more → Jan 7, 2026

What are the accounting standards for lease contracts (IFRS 16)?

IFRS 16 requires lessees to recognize most leases on balance sheet as Right-of-Use assets and lease liabilities. Lessors continue to classify leases as operating or finance.

Read more → Jan 7, 2026

What is the content and presentation of financial statements according to IAS 1?

IAS 1 requires: Statement of Financial Position, Statement of Profit/Loss and OCI, Statement of Changes in Equity, Statement of Cash Flows, Notes, prepared with fair presentation and going concern basis.

Read more → Jan 7, 2026

What is the objective of International Financial Reporting Standards (IFRS)?

IFRS objective: provide financial information useful to existing/potential investors, lenders, and creditors in making decisions about providing resources to the entity.

Read more → Jan 7, 2026

What is the General Ledger? What is a Trial Balance?

The General Ledger is the master set of accounts summarizing all transactions, while a Trial Balance is a worksheet listing all ledger accounts and their balances to prove mathematical equality.

Read more → Jan 7, 2026

What is Goodwill? How does it appear on the balance sheet? And when is it tested for impairment?

Goodwill is an intangible asset arising from business acquisitions when purchase price exceeds fair value of identifiable net assets. It appears as a non-current asset and is tested for impairment annually.

Read more → Jan 7, 2026

How are intangible assets valued and impaired (Goodwill, Patents)?

Intangible assets are initially valued at cost and subsequently amortized (finite life) or tested for impairment (indefinite life). Goodwill and intangible assets with indefinite lives are tested annually for impairment.

Read more → Jan 7, 2026

What are provisions (Provision for Doubtful Debts, Provision for Inventory Obsolescence)?

Provisions are liabilities of uncertain timing or amount, recognized when a present obligation exists from a past event, an outflow is probable, and a reliable estimate can be made.

Read more → Jan 7, 2026

What is the cost of inventory? What items are included in it?

Inventory cost includes all costs necessary to bring inventory to its present location and condition ready for sale, including purchase price, import duties, transportation, and conversion costs for manufactured goods.

Read more → Jan 7, 2026

What is the difference between FIFO and LIFO, and what is the effect of each on net income during periods of inflation?

FIFO (First-In, First-Out) assumes oldest inventory sold first, while LIFO (Last-In, First-Out) assumes newest inventory sold first. During inflation, FIFO results in lower COGS and higher net income, while LIFO results in higher COGS and lower net income.

Read more → Jan 7, 2026

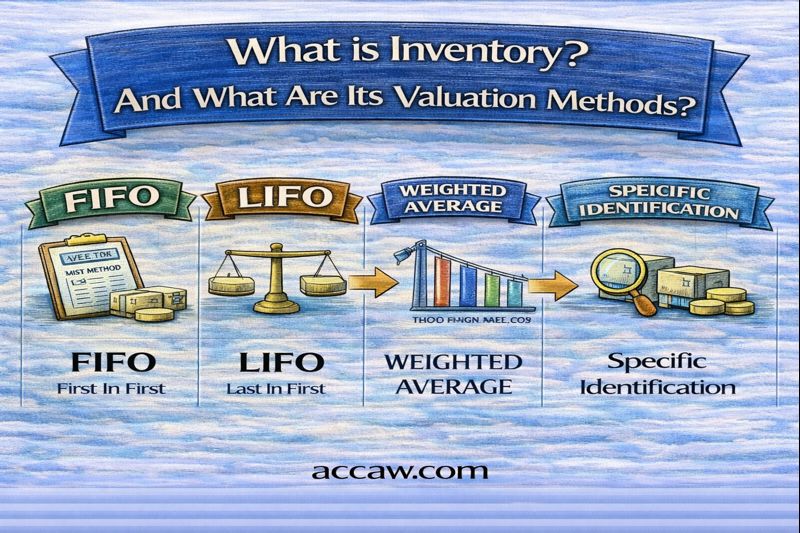

What is inventory? What are its valuation methods (FIFO, LIFO, Weighted Average, Specific Identification)?

Inventory refers to goods held for sale or production. Valuation methods include FIFO, LIFO, Weighted Average, and Specific Identification, affecting cost of goods sold and ending inventory values.

Read more → Jan 7, 2026

How is the purchase, depreciation, and sale of an asset recorded?

Asset transactions involve initial purchase recording, periodic depreciation entries, and sale recording with gain/loss recognition when the asset is disposed of.

Read more → Jan 7, 2026

What is the difference between Depreciation, Amortization, and Depletion?

Depreciation applies to tangible fixed assets, amortization to intangible assets, and depletion to natural resources - all methods of allocating asset costs over useful lives.

Read more → Jan 7, 2026

What are the methods of depreciating fixed assets? (Straight-line, Declining Balance, Units of Production) and which is preferred and why?

Common depreciation methods include Straight-line, Declining Balance, and Units of Production. The preferred method depends on how the asset's benefits are consumed over time.

Read more → Jan 7, 2026

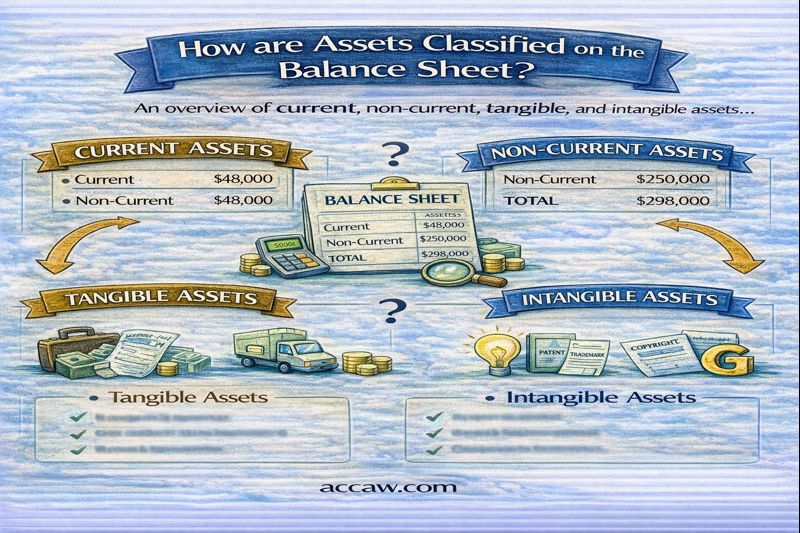

How are assets classified on the balance sheet (current/non-current, tangible/intangible)?

Assets are classified as current/non-current based on liquidity and tangible/intangible based on physical existence, providing useful information about a company's financial position.

Read more → Jan 7, 2026

What is the double-entry system?

The double-entry system is the standard bookkeeping method where every financial transaction affects at least two accounts in equal and opposite ways, maintaining the accounting equation balance.

Read more → Jan 7, 2026

What are common accounting errors and how are they corrected?

Common accounting errors include omission, commission, principle, original entry, and reversal errors, each requiring specific correction methods through journal entries.

Read more → Jan 7, 2026

What is the difference between capital repairs and revenue repairs for fixed assets?

Capital repairs (CAPEX) enhance assets or extend useful life and are capitalized, while revenue repairs maintain existing capacity and are expensed immediately.

Read more → Jan 7, 2026

What are accounting journal entries? What are their types (daily, adjusting, closing)?

Journal entries are the formal record of financial transactions expressed in debits and credits, recorded chronologically in the general journal. Main types include daily, adjusting, and closing entries.

Read more → Jan 7, 2026

What is the difference between accrued revenues and unearned (deferred) revenues?

Accrued revenues are assets representing revenue earned but not yet received, while unearned revenues are liabilities representing cash received for services not yet provided.

Read more → Jan 7, 2026

What is the difference between prepaid expenses and accrued expenses?

Prepaid expenses are assets representing payments made in advance, while accrued expenses are liabilities representing expenses incurred but not yet paid or recorded.

Read more → Jan 7, 2026

Explain the accounting cycle from the initial entry to the preparation of financial statements.

The accounting cycle is a collective process of identifying, analyzing, and recording accounting events over an accounting period, culminating in financial statement preparation.

Read more → Jan 7, 2026

What is the concept of "Prudence" (Conservatism) in accounting?

Prudence (Conservatism) advises exercising caution when making judgments under uncertainty, so that assets or income are not overstated, and liabilities or expenses are not understated.

Read more → Jan 7, 2026

What is the concept of "Materiality"?

Materiality is an accounting concept that states financial information is material if omitting, misstating, or obscuring it could reasonably be expected to influence the economic decisions of users.

Read more → Jan 7, 2026

What are the qualitative characteristics of useful financial information (Relevance, Reliability, etc.)?

Useful financial information must possess fundamental qualitative characteristics: Relevance and Faithful Representation, along with enhancing characteristics like Comparability, Verifiability, Timeliness, and Understandability.

Read more → Jan 7, 2026

Explain the accrual basis of accounting and compare it to the cash basis

Accrual basis records transactions when they occur (revenues when earned, expenses when incurred), while cash basis records only when cash is received or paid.

Read more → Jan 7, 2026

What are the main accounting principles (Historical Cost, Matching, Revenue Recognition, etc.)?

The main accounting principles guide how transactions are recorded and reported. These include Historical Cost Principle, Revenue Recognition Principle, Matching Principle, and Full Disclosure Principle.

Read more → Jan 7, 2026

What are the main accounting assumptions (Going Concern, Accounting Entity, etc.)?

The main accounting assumptions provide a foundational framework for preparing financial statements. Key assumptions include Going Concern, Accounting Entity, Monetary Unit, and Time Period assumptions.

Read more → Jan 7, 2026

Explain the fundamental accounting equation (Assets = Liabilities + Equity)

The fundamental accounting equation is: Assets = Liabilities + Owner's Equity. It is the foundation of the double-entry bookkeeping system and must always be in balance.

Read more → Jan 7, 2026

What are the components of equity (Share Capital, Preferred Shares, Common Shares, Retained Earnings, Treasury Shares)?

Equity components include Share Capital (Common/Preferred Shares), Retained Earnings, Treasury Shares, and Other Comprehensive Income, representing owners' residual claim on assets.

Read more → Jan 7, 2026

What are the criteria for revenue recognition (according to IFRS 15)?

IFRS 15 uses a five-step model: 1) Identify contract, 2) Identify performance obligations, 3) Determine transaction price, 4) Allocate price to obligations, 5) Recognize revenue when obligations are satisfied.

Read more → Jan 7, 2026

What is the matching principle (of revenues and expenses)?

The matching principle states that expenses should be recognized in the same accounting period as the revenues they helped to generate, ensuring proper net income calculation.

Read more → Jan 7, 2026

What is the difference between expenses and losses?

Expenses are costs incurred in ordinary business activities (core operations), while losses result from peripheral or incidental transactions not related to primary operations.

Read more → Jan 7, 2026

What is the difference between revenues and gains?

Revenues arise from ordinary business activities (core operations), while gains result from peripheral or incidental transactions not related to primary operations.

Read more → Jan 7, 2026

What is the structure of the income statement (single-step vs. multi-step)?

Single-step income statement groups all revenues and expenses together, while multi-step separates operating from non-operating activities and shows intermediate profit measures like gross profit and operating income.

Read more → Jan 7, 2026

How are basic and diluted earnings per share (EPS) calculated?

Basic EPS = (Net Income - Preferred Dividends) / Weighted Average Shares. Diluted EPS includes potential dilutive securities like options, convertible bonds, and convertible preferred stock.

Read more → Jan 7, 2026

What is the difference between employee stock options and restricted stock?

Stock options give the right to buy shares at a set price, while restricted stock grants actual shares subject to vesting conditions. Both are equity-based compensation with different accounting treatments.

Read more → Jan 7, 2026

What is the Statement of Changes in Equity?

The Statement of Changes in Equity explains changes in a company's equity over a period, showing effects of net income, other comprehensive income, owner contributions/distributions, and other changes.

Read more → Jan 7, 2026

What are retained earnings? How does its balance change?

Retained earnings represent cumulative net income retained in the business (not distributed as dividends). It increases with net income and decreases with net losses and dividends.

Read more → Jan 7, 2026

What is the contribution margin? How is it calculated?

Contribution margin is revenue minus variable costs, representing the amount contributing to covering fixed costs and generating profit. Calculated as Selling Price - Variable Cost per unit.

Read more → Jan 7, 2026

How is the issuance of shares, purchase of treasury shares, and reissue of treasury shares recorded?

Share issuance records capital contributions, treasury share purchases reduce equity, and reissues may create gains/losses in equity accounts, not affecting the income statement.

Read more → Jan 7, 2026

What is the difference between cash dividends and stock dividends?

Cash dividends distribute cash to shareholders, reducing assets and equity, while stock dividends distribute additional shares, reallocating equity between accounts without affecting total equity.

Read more → Jan 7, 2026

What is accounting? And what is the difference between accounting and bookkeeping?

Accounting is the systematic process of identifying, recording, measuring, classifying, verifying, summarizing, interpreting, and communicating financial information. It provides a clear picture of the financial health of an organization to its various stakeholders.

Read more → Jan 7, 2026

What is the difference between provisions and contingent liabilities? How are they presented in the financial statements?

Provisions are recognized liabilities (probable outflow), while contingent liabilities are possible obligations (not probable) or present obligations that cannot be measured reliably.

Read more → Jan 7, 2026

What are provisions for liabilities (provision for warranties, provision for pensions)?

Provisions for liabilities are estimated obligations of uncertain timing/amount, recognized when a present obligation exists from a past event and an outflow is probable and measurable.

Read more → Jan 7, 2026

What are unearned revenues (deferred revenues)? How are they accounted for?

Unearned revenue (deferred revenue) is cash received in advance for goods/services not yet delivered. It is recorded as a liability and recognized as revenue when performance obligations are satisfied.

Read more → Jan 7, 2026

What are accrued expenses? Give examples.

Accrued expenses are expenses that have been incurred but not yet paid or recorded by period-end, requiring adjusting entries to comply with the matching principle.

Read more → Jan 7, 2026

How is the issuance of bonds at a premium or discount recorded and how is that premium/discount amortized?

Bonds issued at premium (price > face value) or discount (price < face value) require amortization of the premium/discount over the bond life using the effective interest method.

Read more → Jan 7, 2026

What is the difference between Bonds Payable and Notes Payable?

Bonds Payable are long-term debt instruments issued to the public, often traded on markets, while Notes Payable are typically shorter-term loans from banks or financial institutions.

Read more → Jan 7, 2026

How are liabilities classified (current/non-current)?

Liabilities are classified as current (settled within one year or operating cycle) or non-current (settled after one year) based on their due date or maturity.

Read more → Jan 7, 2026

What is an impairment test for assets and how is it performed?

Impairment testing ensures assets are not carried above their recoverable amount. It involves comparing carrying amount to recoverable amount (higher of fair value less costs to sell and value in use).

Read more → Jan 7, 2026

What are biological assets? How are they accounted for?

Biological assets are living animals or plants controlled by an entity. Under IAS 41, they are measured at fair value less costs to sell at each reporting date, with changes recognized in profit or loss.

Read more → Jan 7, 2026

How are investments in shares of other companies accounted for (at Fair Value, using the Equity Method)?

Investments are accounted for based on level of influence: Fair Value Through Profit/Loss (no significant influence), Fair Value Through OCI (elective), Equity Method (significant influence), or Consolidation (control).

Read more → Jan 7, 2026

What is the difference between an operating lease and a finance (capital) lease?

Under old standards, operating leases were rentals while finance leases were essentially purchases. Under IFRS 16/ASC 842, most leases are now treated as finance leases for lessees.

Read more → Jan 7, 2026