What are the methods for allocating indirect costs to cost centers?

Cost Allocation

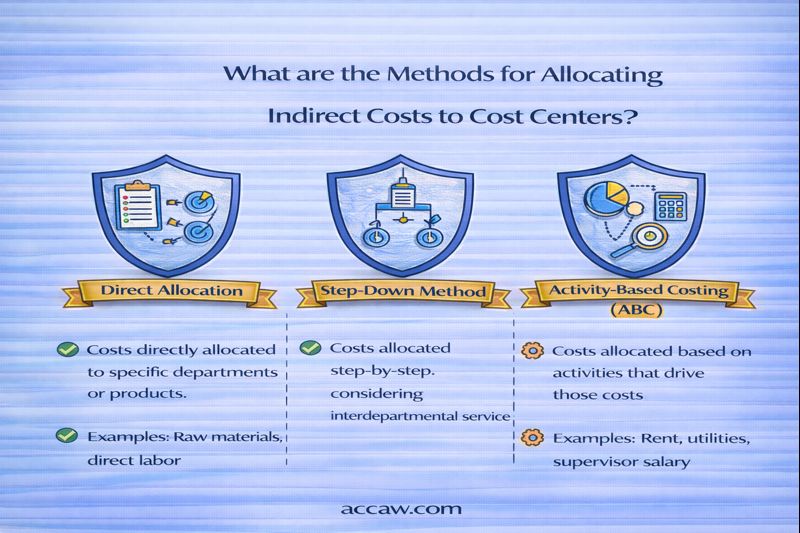

What are the methods for allocating indirect costs to cost centers?

Summary: Indirect costs (overhead) are allocated to cost centers (departments, products) using an allocation base that approximates the cause-and-effect relationship or benefit received. Common traditional methods include: Direct Labor Hours, Direct Labor Cost, Machine Hours, Units of Production, and Square Footage. Activity-Based Costing (ABC) is a more refined method that uses multiple cost drivers based on activities.

The Art (and Science) of Fair Allocation

Since indirect costs cannot be traced, allocation is necessary to assign them to cost objects for product costing, profitability analysis, and decision-making. The goal is to use a base that best reflects how the cost is consumed.

1. Traditional Single-Rate Allocation Methods

These methods use one plant-wide overhead rate or departmental rates.

A. Direct Labor Hours (DLH)

Overhead Rate = Total Estimated Overhead / Total Estimated Direct Labor Hours Overhead Allocated to Product = DLH used by Product × Overhead Rate

When to use: Labor-intensive operations where overhead correlates with labor time.

B. Direct Labor Cost (DLC)

Overhead Rate = Total Estimated Overhead / Total Estimated Direct Labor Cost (as a %) Overhead Allocated to Product = DLC of Product × Overhead Rate

When to use: Similar to DLH, but when wage rates vary significantly across departments/products.

C. Machine Hours

Overhead Rate = Total Estimated Overhead / Total Estimated Machine Hours Overhead Allocated to Product = Machine Hours used by Product × Overhead Rate

When to use: Highly automated, capital-intensive environments where overhead (depreciation, power) is driven by machine usage.

D. Units of Production

Overhead Rate = Total Estimated Overhead / Total Estimated Units of Output Overhead Allocated to Product = Units of Product × Overhead Rate

When to use: When all products are very similar and consume overhead in a uniform way (simple process costing).

E. Square Footage (for facility costs)

Cost per sq. ft. = Total Facility Costs (rent, utilities) / Total Square Footage Allocated to Dept. = Dept. Square Footage × Cost per sq. ft.

When to use: Allocating occupancy costs to departments based on space used.

2. Activity-Based Costing (ABC): A Multi-Driver Approach

ABC recognizes that different overhead costs are driven by different activities, not just one volume-based measure.

- Identify Activities: (e.g., machine setup, quality inspection, purchase ordering).

- Assign Costs to Activity Cost Pools: Accumulate overhead costs for each activity.

- Identify Cost Drivers: For each activity, find a measurable factor that causes the cost (e.g., number of setups, number of inspections, number of orders).

- Calculate Activity Rates: Rate = Total Cost in Pool / Total Cost Driver Units.

- Assign Costs to Cost Objects: For each product, multiply the activity rate by the amount of the cost driver it consumed.

Example: A complex, low-volume product that requires many setups will be assigned more setup costs under ABC than under a traditional labor-hour method, leading to more accurate costing.

3. Choosing an Allocation Method: Key Considerations

- Cause-and-Effect Relationship: Does the base reflect how the cost is incurred? (Most important).

- Benefits Received: Does the cost object benefit from the cost in proportion to the base?

- Fairness/Equity: In service departments (IT, HR) allocating to operating departments.

- Cost and Ease of Use: Simpler methods are cheaper to implement.

- Behavioral Effects: The method can influence manager behavior (e.g., using machine hours may discourage machine use).

4. Practical Example: Comparing Methods

Data: Total MOH: $500,000. Total DLH: 100,000 hrs. Total Machine Hrs: 50,000 hrs.

Product X uses 2 DLH and 1 Machine Hour per unit.

DLH Rate: $500,000 / 100,000 hrs = $5 per DLH. Allocated to X: 2 hrs × $5 = $10/unit Machine Hr Rate: $500,000 / 50,000 hrs = $10 per MH. Allocated to X: 1 hr × $10 = $10/unit

In this case, both give the same result. But if Product Y used 1 DLH and 3 Machine Hours, the allocated cost would differ significantly, highlighting the importance of choosing the right driver.

5. Conclusion: From Rough Estimates to Refined Accuracy

Traditional allocation methods provide a simple, cost-effective way to assign overhead, but they can distort costs if the single base doesn't reflect actual consumption. ABC provides more accuracy for complex, diverse product lines but is more costly to implement. The choice depends on the diversity of products, the importance of accurate cost information for decisions, and the cost-benefit trade-off.