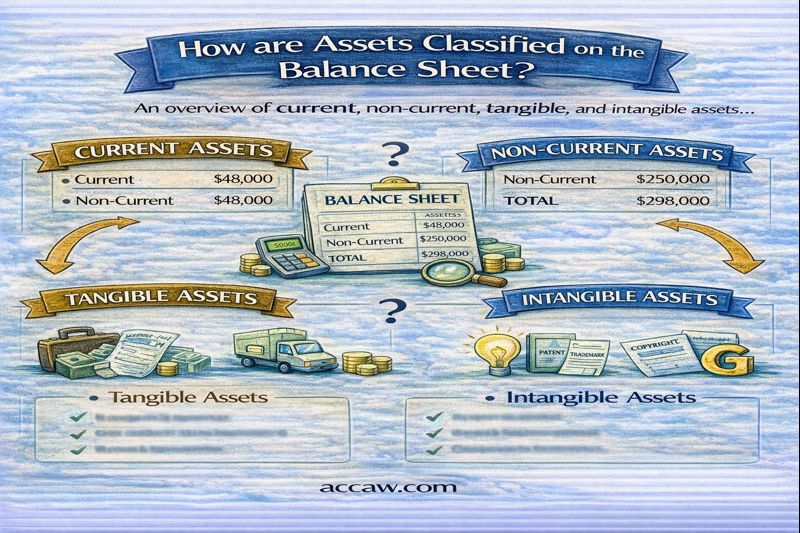

2. Classification by Physical Nature

Tangible Assets:

Physical assets that can be touched and seen.

- Characteristics: Physical substance, depreciable

- Examples:

- Land

- Buildings

- Machinery & Equipment

- Vehicles

- Furniture & Fixtures

- Accounting: Depreciated (except land)

Intangible Assets:

Non-physical assets without physical substance.

- Characteristics: No physical form, identifiable

- Examples:

- Patents

- Trademarks

- Copyrights

- Software

- Goodwill (unidentifiable intangible)

- Accounting: Amortized (finite life) or impairment tested (indefinite life)

Special Categories:

Property, Plant & Equipment (PPE):

- Tangible assets used in operations

- Presented at cost less accumulated depreciation

- Disclose separately: Land, Buildings, Equipment

Financial Assets:

- Investments in securities

- Classified as: Trading, Available-for-sale, or Held-to-maturity

- Current vs non-current based on holding period

Other Assets:

- Deferred tax assets

- Prepaid expenses (long-term portion)

- Security deposits

Key Accounting Standards:

- IAS 1: Requires current/non-current classification

- IAS 16: Property, Plant and Equipment

- IAS 38: Intangible Assets

- IAS 36: Impairment of Assets

Important Considerations:

- Materiality: Significant items disclosed separately

- Consistency: Same classification method each period

- Judgment: Some assets may be current or non-current depending on use

- Disclosures: Must disclose basis of classification

- Reclassification: If asset's use changes, may need to reclassify

Financial Analysis Implications:

Current Ratio Analysis:

Current Ratio = Current Assets ÷ Current Liabilities

- Higher ratio indicates better short-term liquidity

- Industry norms vary (retail vs manufacturing)

Asset Turnover Ratios:

- Total Asset Turnover: Sales ÷ Total Assets

- Fixed Asset Turnover: Sales ÷ Net Fixed Assets

- Measures efficiency of asset use

Capital Structure Analysis:

- Proportion of fixed vs current assets

- High fixed assets may indicate capital-intensive business

- Intangible-heavy companies may have different risk profiles

Common Classification Challenges:

- Inventory: May be long-term if held for sale beyond one year

- Prepaid Expenses: Split between current and non-current portions

- Investments: Classification depends on management intent

- Assets Held for Sale: Separate category with special rules

- Leased Assets: Right-of-use assets under IFRS 16

Best Practices for Asset Classification:

- Establish clear classification policies

- Regularly review asset useful lives

- Document rationale for classification decisions

- Ensure consistency across reporting periods

- Train accounting staff on classification rules

- Review industry practices for comparability

Practical Example - Manufacturing Company:

- Current Assets:

• Cash: $100,000

• Raw Materials: $50,000

• Work-in-Progress: $30,000

• Finished Goods: $70,000

• Accounts Receivable: $150,000

- Non-Current Assets:

• Land: $200,000

• Factory Building: $500,000

• Machinery: $300,000

• Patents: $100,000

• Goodwill: $50,000

Key Takeaways:

- Classification provides vital information about liquidity and asset composition

- Must follow accounting standards (IFRS/GAAP) requirements

- Affects financial ratios and analysis

- Requires professional judgment for certain assets

- Proper classification enhances financial statement usefulness

- Regular review and updates needed as business changes