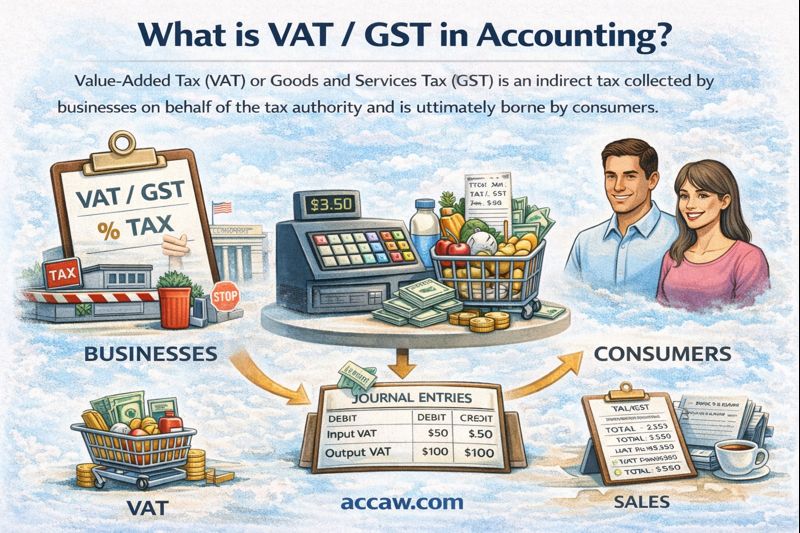

1) What is VAT / GST in accounting?

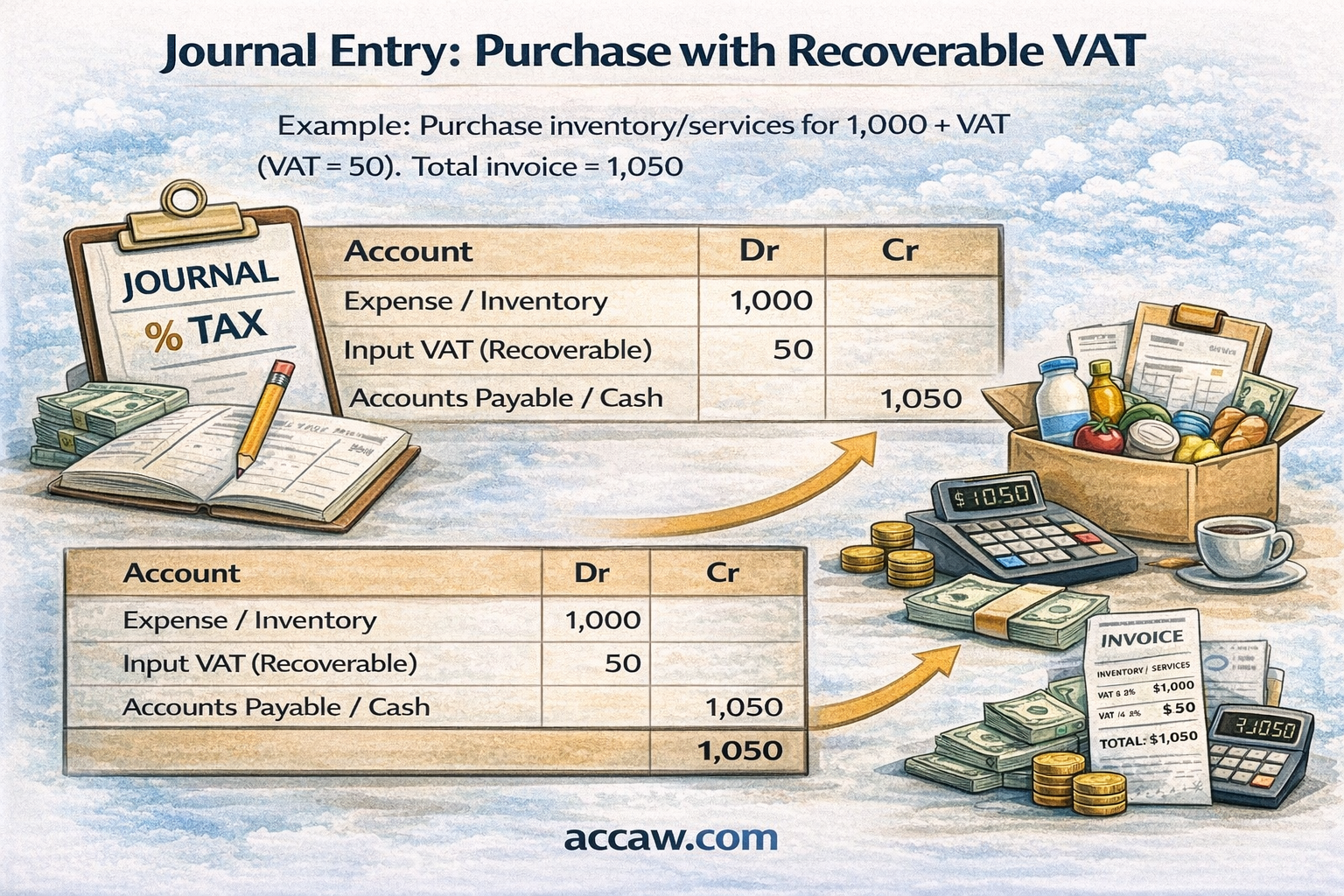

VAT/GST is an indirect tax collected by businesses on behalf of the tax authority. In most systems, the business:

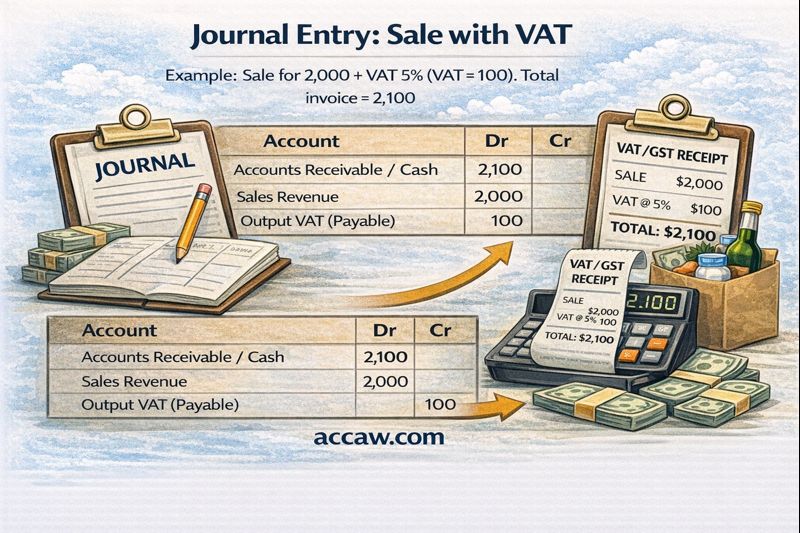

- Charges VAT/GST on sales (Output VAT)

- Pays VAT/GST on purchases (Input VAT)

The net amount (Output − Input) is typically paid to or refunded from the tax authority.